- Version

- Download 13

- File Size 3.15 MB

- File Count 1

- Create Date August 6, 2025

- Last Updated August 6, 2025

Construction Monitor July 2025

Western Cape Surges Ahead While National Growth Stalls

South Africa’s economic outlook remained fragile in July 2025, amid muted growth expectations, lingering inflationary pressures, and persistent structural challenges. The IMF maintained a subdued growth forecast of just 1.0% for 2025, with real GDP growth continuing to be held back by inefficiencies in energy, transport, and governance across state-owned entities. Although headline inflation remained within the SARB's target range at 3.0%, cost pressures from food, housing, and regulated prices were evident. Manufacturing activity showed early signs of recovery, with the Absa PMI rising above 50 for the first time in nine months, driven by stronger new orders and export demand. Mining production also edged up slightly, supported by robust iron ore output and a sharp rise in gold sales. However, wholesale trade remained weak, and retail growth was uneven—reflecting still-fragile consumer and business confidence despite interest rate stability and temporary currency gains.

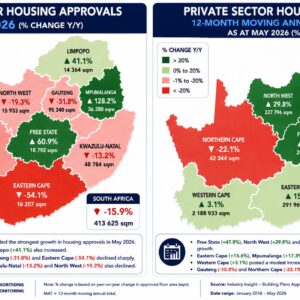

In the construction and infrastructure sector, development momentum remained highly uneven across the provinces. The Western Cape stood out with its decisive infrastructure push, including a R71 billion grid upgrade programme, the launch of the R2 billion Founders Garden housing project, and preparations for a second international airport. In KwaZulu-Natal, infrastructure efforts centred on the R450 million Mpophomeni Wastewater Treatment Works and continued investment in the Dube TradePort SEZ. Gauteng advanced several high-impact projects, including a R2.5 billion AfDB-backed loan for Johannesburg’s urban infrastructure. Yet progress was undermined by service delivery failures, rising irregular expenditure, and mounting contractor performance issues. Meanwhile, in provinces such as the Eastern Cape, Limpopo, and Mpumalanga, infrastructure efforts were marred by sabotage, stalled projects, and community unrest, reflecting deep-seated governance and service delivery failures.

Overall, South Africa’s infrastructure and economic trajectory in July 2025 highlighted a growing divergence between regions demonstrating policy coherence and investor confidence—such as the Western Cape—and others plagued by operational dysfunction. With public sector budgets under strain and structural bottlenecks unresolved, sustaining growth and development will increasingly depend on institutional reform, improved project delivery, and deeper private sector participation.

Attached Files

| File | |

|---|---|

| Construction Monitor July 2025.pdf |