- Version

- Download 2

- File Size 908.34 KB

- File Count 1

- Create Date August 6, 2025

- Last Updated August 6, 2025

Preferred Construction Material Supplier and Competitor Survey July 2025

The Preferred Supplier & Competitor Survey (PSS) – June 2025 provides detailed insights into the market exposure, contractor feedback, project delays, and risks affecting South Africa’s construction materials sector.

Public Sector Delays and Skills Shortages Stall Progress Despite R11bn in New Awards

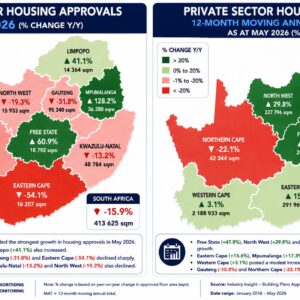

The July 2025 Preferred Supplier and Competitor Survey (PSS) report provides insights into construction activity and material supplier dynamics across South Africa. It is based on a sample of 13 projects worth approximately R1.2 billion, mostly awarded in late 2024, with a focus on education, housing, and road infrastructure. Key observations highlight delays due to late payments, political interference, community disruptions, and a shortage of skilled project managers, especially in provinces like KwaZulu-Natal, Limpopo, and the Free State.

The report tracks the Market Exposure Rate (MER) of construction material suppliers, gauging their participation based on project value. Construction material prices remained relatively stable, with no major price hikes reported, though G1 stone remains in short supply. The use of imported cement (notably Simba Cement from Vietnam) is increasing, particularly in KwaZulu-Natal. In terms of supplier recognition, firms like AfriSam and Chryso SA were praised for quality and service in the Western Cape.

On the construction activity front, R11.1 billion in project awards were recorded in June 2025, a 53% increase from May and 54% higher year-on-year, mostly driven by civil projects (R9.2bn). However, building project awards declined 54% y/y. Civil activity was most prominent in Limpopo, Gauteng, Mpumalanga, and the Northern Cape, while tender activity fell sharply by 65% y/y, with only 197 tenders issued.

In summary, while construction project awards surged, the industry continues to face operational and funding challenges, regional disparities in activity, and fragile supplier-contractor relationships, especially in the public sector.

Attached Files

| File | |

|---|---|

| PSS Overview July 2025.pdf |