- Version

- Download 2

- File Size 864.54 KB

- File Count 1

- Create Date July 3, 2025

- Last Updated July 3, 2025

Preferred Construction Material Supplier and Competitor Survey June 2025

The Preferred Supplier & Competitor Survey (PSS) – June 2025 provides detailed insights into the market exposure, contractor feedback, project delays, and risks affecting South Africa’s construction materials sector.

Slow Recovery in Building Projects as Provinces Grapple with Delays and Cancellations

Based on a survey of 63 projects worth R4.78 billion (mostly awarded in late 2024), the report focuses on supplier participation through Market Exposure Rates (MER), with a particular emphasis on sectors like education, housing, and roads. A 42% contractor response rate was achieved, but reluctance to participate—especially in KwaZulu-Natal, Limpopo, and the North West Province, highlights ongoing issues with delayed payments, confidentiality concerns, and project suspensions.

The report highlights severe challenges in the Eastern Cape, where a construction manager was kidnapped in an incident possibly linked to the “construction mafia,” emphasizing growing security risks and contractor hesitancy to share data. Despite these tensions, some progress was noted in social housing projects as payment processes improved. Material shortages, particularly for electrical conduit in Mpumalanga, and brand-specific cement use across provinces (e.g., PPC’s IDM and iTe’s Pharoah cement) reflect ongoing supply chain adjustments.

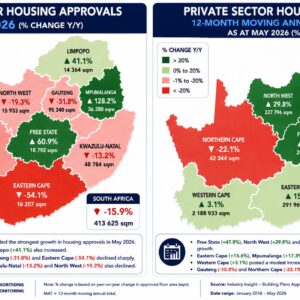

Nationally, 757 projects valued at R97.9 billion were surveyed over the past 12 months, marking a 31% increase in project value despite a 2.7% decline in project count. Construction material price inflation slowed sharply, with the composite index turning deflationary at -0.3% in May 2025, due to price drops in steel, cement, and bitumen. Concurrently, May saw a significant 50% drop in awarded project value compared to April (R5.9 billion total), though year-on-year values were up 11.7%. Civil works dominated, especially in the Western and Eastern Cape, while building activity rose in KZN, Gauteng, and Eastern Cape. The number of tenders and cancellations also declined sharply year-on-year, reflecting growing uncertainty in the construction pipeline.

Overall, the report paints a picture of a sector under pressure from payment delays, criminal activity, reduced tender volumes, and increased contractor disengagement—yet showing signs of resilience in certain provinces and material categories.

Attached Files

| File | |

|---|---|

| PSS Overview June 2025.pdf |