- Version

- Download 16

- File Size 2.75 MB

- File Count 1

- Create Date July 4, 2025

- Last Updated July 4, 2025

Construction Monitor June 2025

Strong gains in Turnover, but Lacklustre Private Sector and Public Tender Slowdown Weigh on Sector

South Africa’s economy remained deeply fragile in June 2025, with weak growth, deteriorating business confidence, and persistent structural constraints undermining recovery prospects. Sharp contractions in manufacturing (-6.3% y/y) and mining (-7.7% y/y), particularly in platinum group metals (-24.1%), weighed heavily on output. Retail trade showed selective resilience, but hardware and building materials sales stayed deeply negative. While inflation remained subdued (headline CPI at 2.8% in May), prompting debate around lowering the inflation target, critics warned this could risk entrenching restrictive policy in an already stagnant environment. Fiscal support from multilateral institutions provided a temporary boost, yet GDP forecasts were revised down to between 0.8% and 1.2% for 2025. Structural reforms in governance, infrastructure, and labour markets remain critical to reversing prolonged economic stagnation.

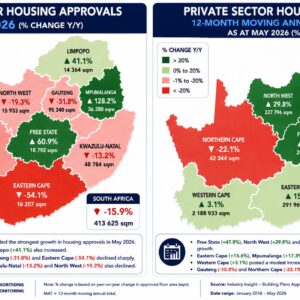

The construction sector reflected these broader pressures. Despite achieving robust growth in construction turnover for the second consecutive quarter in Q1 2025 (contradicting gross fixed capital formation estimates), a lacklustre public infrastructure pipeline due to under-expenditure and institutional delays, weigh in on the construction outlook. Private residential building approvals slowed significantly with double digit declines in completions. Public sector building and civil activity is severely constrained by fiscal limits and project inefficiencies. Listed construction and materials companies reflected subdued market sentiment, with the CRMS Index slipping in June and share price recovery lagging pre-2022 levels. Although a few mid-sized players saw earnings growth, overall investor caution prevails amid delays, cost pressures, and weak demand. Provincial trends continue to diverge: the Western Cape outperformed thanks to strong local governance and inward migration, while Gauteng’s private sector demand softened. KwaZulu-Natal and the Eastern Cape remained the weakest regions, hindered by poor procurement and low project execution capacity.... Download the full monthly review here (available to Subscribers)

Attached Files

| File | |

|---|---|

| Construction Monitor June 2025.pdf |