- Version

- Download 5

- File Size 925.86 KB

- File Count 1

- Create Date September 2, 2025

- Last Updated September 2, 2025

Preferred Construction Material Supplier and Competitor Survey August 2025

The Preferred Supplier & Competitor Survey (PSS) – August 2025 provides detailed insights into the market exposure, contractor feedback, project delays, and risks affecting South Africa’s construction materials sector.

Signs of Recovery in Gauteng, Yet Systemic Risks Persist Across Provinces

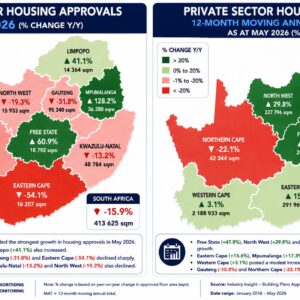

The August 2025 survey reflected a mixed but generally active market, with 124 projects worth an estimated R32.7 billion reviewed. Contractor participation improved and reached 77%, with notable activity across education, housing, and road sectors. However, delayed payments, weather disruptions, and community interference continued to hinder progress, especially in KwaZulu-Natal where multiple housing, education, and health projects faced stoppages or extensions due to payment backlogs. Limpopo’s construction activity was supported by major infrastructure upgrades around Polokwane, including water, roads, and housing projects, although material availability challenges, particularly bricks and cement, forced contractors to rely on suppliers outside the province. In Gauteng, signs of renewed growth were evident, especially in commercial and logistics developments, with tower cranes reappearing across Sandton, Rosebank, and Midrand after years of stagnation, though disputes over BOQs, vandalism, and security concerns persisted.

Contractor responses highlighted ongoing systemic challenges within the industry. In the Eastern Cape, project funding shortfalls and deliberate underpricing of tenders were reported, leading to abandoned works and stop-start completion contracts. Free State contractors raised concerns over slow tendering processes and difficulties in sourcing aggregates, though innovative cement application methods were helping to reduce material costs. The survey confirmed that while civil sector awards remained dominant, driven by large projects in Mpumalanga, Western Cape, and Gauteng, the building sector recorded weaker activity. Payment delays, material shortages, and community disruptions continue to weigh heavily on contractors’ ability to deliver, yet isolated signs of private sector-driven recovery, particularly in Gauteng, suggest some resilience within the industry despite persistent structural risks.

Attached Files

| File | |

|---|---|

| PSS Overview August 2025.pdf |