- Version

- Download 9

- File Size 2.97 MB

- File Count 1

- Create Date June 9, 2025

- Last Updated June 9, 2025

Construction Monitor May 2025

Construction Sector Strains Under Policy Delays, Despite Investment Hopes and Rising Tender Awards

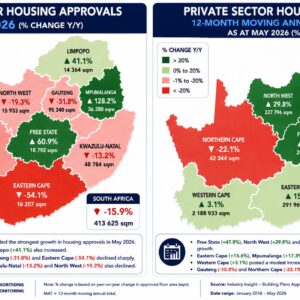

South Africa’s construction sector in May 2025 continued to reflect a dichotomy between renewed investment optimism and deep-rooted structural weaknesses. On one hand, the civil construction market showed notable growth, with project awards exceeding R53 billion in the first four months—driven by large water and transport contracts. National Treasury reaffirmed over R1 trillion in infrastructure allocations in the revised Budget, while major provinces like Gauteng and KwaZulu-Natal announced substantial projects at investment summits. However, the overall construction pipeline shrank by 17.4% year-on-year by March, public building tender values dropped 18%, and delays and cancellations rose sharply. Residential approvals and building material mining volumes also declined, and provinces such as Limpopo, KwaZulu-Natal, and Free State posted pipeline contractions of over 30%.

Economic conditions remain fragile, with GDP growth in Q1 2025 stagnant at 0.1%, weighed down by contractions in mining and manufacturing, although inflation eased to 2.8% in April. Investor sentiment remains constrained by ongoing political uncertainty, the faltering GNU, and governance failures in key provinces. While the private sector shows pockets of resilience, particularly in the Western Cape and segments of the JSE-listed construction and property companies, broader recovery is undermined by non-payments, corruption, procurement delays, and a high reliance on state-driven activity. As the sector awaits the finalisation of Budget 3.0 and reforms to PPP frameworks, a sustainable turnaround will depend on improved execution, investor confidence, and clearer policy direction.

Attached Files

| File | |

|---|---|

| Construction Monitor May 2025.pdf |