Stabilising Economy and Major Infrastructure Commitments Set South Africa on a Cautious Path to Recovery

South Africa’s construction industry entered the final quarter of 2025 amid a cautiously improving economic and investment climate. Macroeconomic indicators reflected stability, headline inflation held at 3.4 percent, the rand strengthened to around R17.3/$, and the Absa Manufacturing PMI climbed back above the 50-point threshold to 52.2, signaling a tentative recovery in industrial demand. A R21.8 billion trade surplus and firmer retail sales underscored resilience in domestic consumption, while the Cabinet’s approval of the R2.23 trillion Integrated Resource Plan (IRP 2025) and the Construction Action Plan marked a decisive policy shift toward infrastructure-led growth. Major investment commitments, including the R230 billion EU clean-energy package, R127 billion Transnet rail and port upgrades, and the US$547 million Tharisa mining expansion, reinforced renewed investor confidence and a more optimistic medium-term outlook.

Despite these positives, the construction sector remained under pressure through mid-2025, as private-sector building activity weakened, and public-sector rollout remained uneven. Building completions and plans passed fell 21 percent and 9 percent y-y respectively, pointing to a subdued project pipeline and delayed capital formation. Public tender values, however, showed signs of improvement, supported by major provincial and national infrastructure initiatives. More than R300 billion in high-impact projects were announced during October alone, led by the R50 billion Port of Gauteng inland logistics hub, Transnet’s R127 billion modernisation drive, and over R90 billion in new “city-building” developments in Gauteng. These announcements, while largely in early feasibility stages, signal a widening pipeline across logistics, housing, and energy infrastructure and a gradual re-engagement of private-sector capital in long-term construction opportunities.

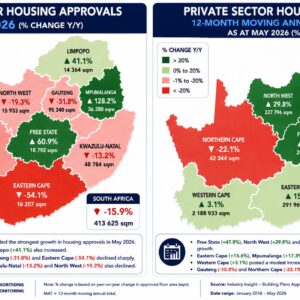

Provincially, performance was mixed: the Western Cape and Gauteng continued to dominate investment activity through large mixed-use, housing, and transport projects, while KwaZulu-Natal recorded nearly R100 billion in investment pledges amid renewed logistics upgrades. By contrast, weaker governance and delivery capacity in provinces such as the Eastern Cape, Free State, Northern Cape, and the North West Province hindered project realisation, with elevated postponement and cancellation rates persisting. Overall, the October 2025 data depict a … Read the full review here (available to subscribers)