- Version

- Download 3

- File Size 937.93 KB

- File Count 1

- Create Date November 4, 2025

- Last Updated November 4, 2025

Preferred Construction Material Supplier and Competitor Survey October 2025

The Preferred Supplier Survey, pioneered by Industry Insight, evaluates the Market Exposure Rate (MER) of key construction material suppliers within the construction industry. MER is used to measure supplier participation in projects based on their exposure to project values rather than sales volumes.

Construction Sector Faces Slow Recovery: Stable Prices and Renewed Tenders Offer Hope Amid Weaker Project Awards

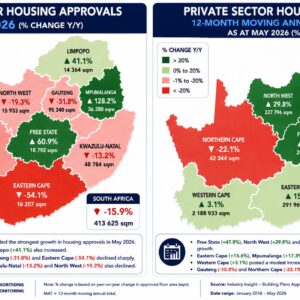

The Preferred Supplier & Competitor Survey (October 2025) highlights continued strain across South Africa’s construction sector, with mixed signals emerging from project data, pricing, and supplier-selection dynamics. The survey covered 208 projects worth roughly R16.8 billion, with participation strongest among contractors in Gauteng and the Western Cape but weaker in KwaZulu-Natal, Limpopo, and North West. Market activity weakened, as the nominal value of construction project awards fell 33 percent y-y to R6.2 billion, led by a 35 percent decline in building awards and a 31 percent fall in civil projects. The Western Cape and Gauteng still accounted for the largest project awards, notably the R781 million Golden Acres redevelopment and R400 million Blackwood Student Accommodation, while KwaZulu-Natal remained the most active province for tenders despite fiscal pressures. Across the public sector, delays, non-payment, and community disruptions continue to plague projects, with several contractors terminating or suspending work due to cash-flow constraints.

On the pricing front, construction-material inflation remained subdued. The composite materials index rose just 1.6 percent y-y in September 2025, well below consumer inflation at 3.1 percent, indicating softer input-cost pressures following years of above-inflation increases. However, selected materials showed renewed volatility — ready-mix concrete rose 1.8 percent m-m, ceiling boards 0.9 %, and rebar prices surged by as much as R1,500 per ton, signaling a potential 10 to11 percent hike in steel costs. Overall, construction cost inflation averaged 0.9 % for 2025 to date, sharply down from 6.1 percent in 2024, creating a relatively stable price environment but offering little relief from weak demand and erratic payment cycles.

In terms of supplier motivation, the survey reaffirmed that professional team specifications remain the dominant driver of material choice, influencing more than 80 percent of decisions across categories. Other factors such as service levels, location, and price competitiveness play secondary roles, while access to credit facilities and transformation considerations remain marginal. The results suggest that despite easing input costs, project delays, tender cancellations, and non-payment continue to constrain contractor confidence and liquidity. With tender activity showing recovery but awards lagging, the October 2025 findings depict a construction industry still in transition — one where price stability and professional influence coexist with chronic delivery challenges and uneven provincial performance.

Download the October 2025 survey results here (available to PSS subscribers)

Attached Files

| File | |

|---|---|

| PSS Overview October 2025.pdf |