- Version

- Download 20

- File Size 2.80 MB

- File Count 1

- Create Date December 11, 2024

- Last Updated December 11, 2024

Construction Monitor November 2024

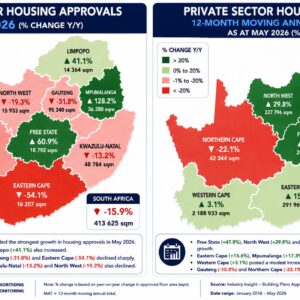

The November 2024 Construction Monitor provides an in-depth analysis of South Africa’s construction sector, presenting a complex mix of challenges and opportunities. The report highlights a significant shift in market dynamics, shaped by both macroeconomic pressures and critical infrastructure needs across the country. Despite a 50-basis-point interest rate cut since September 2024 by the South African Reserve Bank (SARB) with more cuts expected in 2025, the construction sector is experiencing a challenging landscape characterized by a slow pace in private sector recovery, delayed public projects, weak momentum in economic recovery and consistent challenges at local government level.

In this month's report we look at the usual updates including private sector demand for building construction, that showed a promising rebound in September 2024, across various provinces. Public sector building investment, based on tenders that have been released since the election in May continue to disappoint, with a similar trajectory seen in the pace by which the public sector has released tenders for civil construction (with a few provincial exceptions). Economic fundamentals are shifting into what is seen to be a more “investor conducive” gear, and should this momentum continue into 2025, we should start to see a more positive trend in terms of private sector investment in building. However, government not only needs to maintain, but accelerate, the momentum in economic infrastructure to fast track private investment, without losing sight of the desperately needed investment in social infrastructure.

The year 2024 draws to a close with mixed reactions. While we are disappointed that the momentum in 2024 was somewhat lost post-election, an improvement in economic fundamentals with the establishment of the GNU, a gradual revival in business sentiment, lower inflation and lower interest rates, provides the platform of what could be a better 2025.

Although the rate of decline in the value of the construction pipeline has reached double digit rates by September 2024, there could be opportunities that spill over into 2025 following the rapid increase in tender values during the latter part of 2023 and into the first half of 2024, as these projects commence construction. However, there are strong provincial differences and is seen as a broad based, or “blue print fits all” scenario for 2025.

Attached Files

| File | |

|---|---|

| Construction Monitor November 2024.pdf |