- Version

- Download 16

- File Size 2.47 MB

- File Count 1

- Create Date April 17, 2025

- Last Updated April 17, 2025

Construction Monitor March 2025

Recovery on shaky ground: Construction Sector’s early signs of rebound may be short-lived amid political instability and economic uncertainty.

The March 2025 Construction Monitor provides an in-depth analysis of South Africa’s construction sector, presenting a complex mix of challenges and opportunities. The report highlights a significant shift in market dynamics, shaped by both macroeconomic pressures and critical infrastructure needs across the country.

South Africa’s economy is showing mixed signals—retail sales are up, and inflation is stable, but manufacturing, mining, and overall growth remain weak. Political uncertainty, a R16 billion trade deficit (mainly with China), and growing tensions within the Government of National Unity have added to investor unease. Internationally, relations with the U.S. have soured following citrus tariffs and the ambassador’s expulsion, while President Zelenskyy’s upcoming visit highlights South Africa’s complex stance on the Ukraine-Russia conflict.

Domestically, provinces have launched major infrastructure plans, particularly in the Western Cape and Gauteng, though service delivery failures and governance issues persist. Public pressure is mounting on the government to fix state inefficiencies, tackle corruption, and support private investment, but with continued mismanagement and delayed reforms, confidence in South Africa’s economic direction remains fragile.

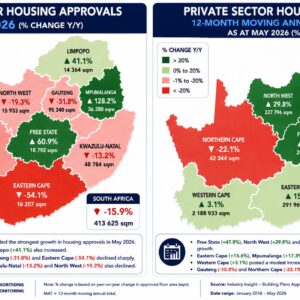

South Africa’s construction sector showed early signs of recovery in January 2025, with a strong rebound in building approvals—up nearly 30% year-on-year—driven by growth in residential and industrial projects, especially in the Western Cape and KwaZulu-Natal. Wholesale and retail sales of construction materials also improved, reflecting more favorable interest rates. However, construction cost inflation is creeping back up, driven by rising material and equipment prices. Despite this progress, the sector remains under pressure: public sector building tenders have declined sharply, project postponements and cancellations—especially in KwaZulu-Natal—are on the rise, and business confidence is being undermined by political instability and global economic uncertainty. Although civil project awards picked up in early 2025 thanks to large SANRAL and uMgeni-uThukela Water contracts, the broader construction pipeline remains fragile, with investor hesitancy and state payment delays limiting long-term momentum.

Download the March 2025 Review here (available to subscribers)

Attached Files

| File | |

|---|---|

| Construction Monitor March 2025.pdf |