- Version

- Download 11

- File Size 2.59 MB

- File Count 1

- Create Date May 9, 2025

- Last Updated May 9, 2025

Construction Monitor April 2025

Investment Pledges, Construction Pipeline cracks, Postponements and Policy Uncertainty.

Summary

The April 2025 Construction Monitor provides an in-depth analysis of South Africa’s construction sector, presenting a complex mix of challenges and opportunities. The report highlights a significant shift in market dynamics, shaped by both macroeconomic pressures and critical infrastructure needs across the country.

South Africa’s economic performance in early 2025 reflects a fragile recovery underpinned by subdued growth, weak industrial output, and mounting policy uncertainty. While inflation dropped to a multi-year low of 2.7% and retail trade remained resilient, the manufacturing and mining sectors continued to contract, with significant declines in building material production and mineral sales. A volatile rand, ongoing global trade tensions, and mixed investor sentiment weigh on the outlook, despite improved foreign direct investment flows and renewed infrastructure commitments from provinces like Gauteng and the Western Cape. Although public investment into logistics and urban development is gaining momentum, governance failures and mismanagement in provinces such as Eastern Cape and KwaZulu Natal continue to undermine broader service delivery and infrastructure reliability.

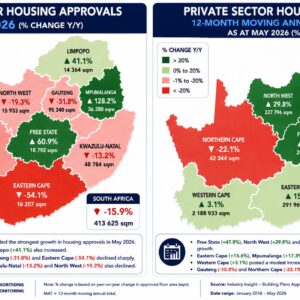

In the construction sector, nominal investment edged up only 0.4% in 2024, with a notable decline in residential activity and a growing reliance on public-led non-residential building. Although tender awards surged to R44.7 billion in the first quarter of 2025, driven by large projects in transport and water, this masks a deeper weakness in the pipeline, marked by project postponements, cancellations, and funding gaps. Building plan approvals fell sharply in February, and public tender values were down across most provinces. High postponement and cancellation rates—particularly in KwaZulu Natal and the North West—reflect the sector’s structural constraints, worsened by political uncertainty, stalled reforms, and a weakening fiscal outlook. As government prepares to table a revised budget in May, concerns are rising that cuts to social infrastructure could further erode momentum in an already pressured construction market....download the April 2025 review here (available to subscribers).

Attached Files

| File | |

|---|---|

| Construction Monitor April 2025.pdf |