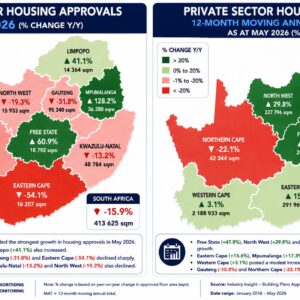

In this month’s monitor we include a “Key Construction Indicator Summary” for the Month, Quarter and Year to Date. We look at the performance of JSE companies involved in the construction sector, the extent of liquidations in the industry, performance of the retail and wholesale trade sales, construction material price inflation, and our usual updates of the performance in the building and civil sectors. As a special feature we include a summary of local governments’ employment costs in relation to operating revenue and how it impacts on capital expenditure. Third quarter GDP performance in terms of construction expenditure disappointed, with total investment in construction having decreased by 1.9 percent y-y in real terms, with a sharper than expected decline in investment in housing (down 4.2 percent) and a surprising decline in construction works where investment declined by 0.9 percent. Growth also slowed in non-residential investment, basically moving sideways with a moderate 0.6 percent increase. Confidence levels amongst civil contractors slowed in the 4th quarter of 2023, from 43 in Q3 to 41. These levels are nothing to get too excited about, but it is a 32 percent improvement from the 4th quarter in 2022. Government’s continued announcements or promises to increase investment in economic infrastructure should start to materialse at some point and while we have seen some improvement in actual expenditure in some local governments, it is clearly still not enough to improve the overall performance in the sector. The outlook for building investment weakened further with another dismal month in terms of approvals for new building construction by the private sector. Click here to download the full review