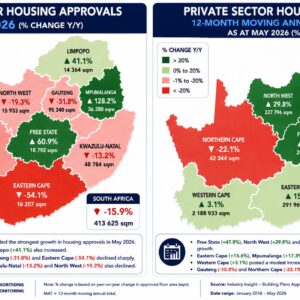

The February/March 2026 Construction Monitor highlights a South African construction sector that remains under pressure despite a relatively supportive macroeconomic backdrop. Inflation has eased to around 3%, supporting consumer activity—particularly retail segments linked to maintenance and renovations, but this resilience is largely confined to household-driven demand. In contrast, investment-led activity remains weak, reflected in declining wholesale trade, reduced construction material volumes, and subdued building material production. The broader economic environment therefore points to a fragmented recovery, where improved consumer conditions are insufficient to stimulate a meaningful rebound in fixed investment or infrastructure delivery. Within the construction sector, activity remains highly uneven across both value chains and geographies. Downstream demand, especially smaller-scale residential maintenance, continues to hold up, while upstream indicators such as bulk procurement, project pipelines and civil awards remain weak. Civil construction activity has deteriorated sharply, with a significant decline in both the value and scale of projects awarded, particularly large (Grade 9) contracts, indicating a constrained pipeline over the short term. Similarly, private sector building approvals continue to contract, especially in residential and industrial segments, reflecting structural affordability constraints, rising development risks, and ongoing municipal inefficiencies. Public sector building activity has also weakened due to budget cuts and constrained fiscal capacity, limiting its ability to offset private sector weakness.

At a provincial level, the report underscores a dual-track infrastructure landscape. The Western Cape, and to a lesser extent KwaZulu-Natal and parts of Gauteng, continue to attract investment and show relative momentum, driven by logistics, mixed-use developments and private sector participation. However, this is increasingly offset by deepening infrastructure and governance failures in other regions—most notably the Eastern Cape, where service delivery breakdowns, procurement inefficiencies and maintenance backlogs are constraining economic activity. Across the country, the key challenge remains the conversion of project pipelines into actual delivery, with institutional capacity, municipal performance and procurement reform emerging as critical constraints.

Cost pressures are also re-emerging as a key risk. Construction material price inflation has accelerated above headline inflation, placing renewed strain on already thin contractor margins in a highly competitive and demand-constrained environment. Combined with rising project cancellations, weak tender activity, and declining investment, the outlook suggests that the construction sector will remain characterised by slow, uneven recovery, with downside risks linked to weak infrastructure delivery, global volatility, and domestic fiscal constraints.

March 2026 Construction Monitor (available to subscribers)